Focus: Renewable Energy Revolution

Joseph Morgan

Population growth, urbanization and technological advancements are leading to an ever increasing appetite for electricity across all regions. Pressure from governments and also environmental activists are requiring the source of this electricity to be both clean and sustainable. These factors are leading to an undeniable disruption in the energy sector with a shift towards renewable energy. This trend is still at its initial innings and will continue to advance over the upcoming years. Through this article we address the current state of renewable energy around the world, and discuss potential investment options for investors looking to take part of this trend.

Growing Electricity Consumption Needs

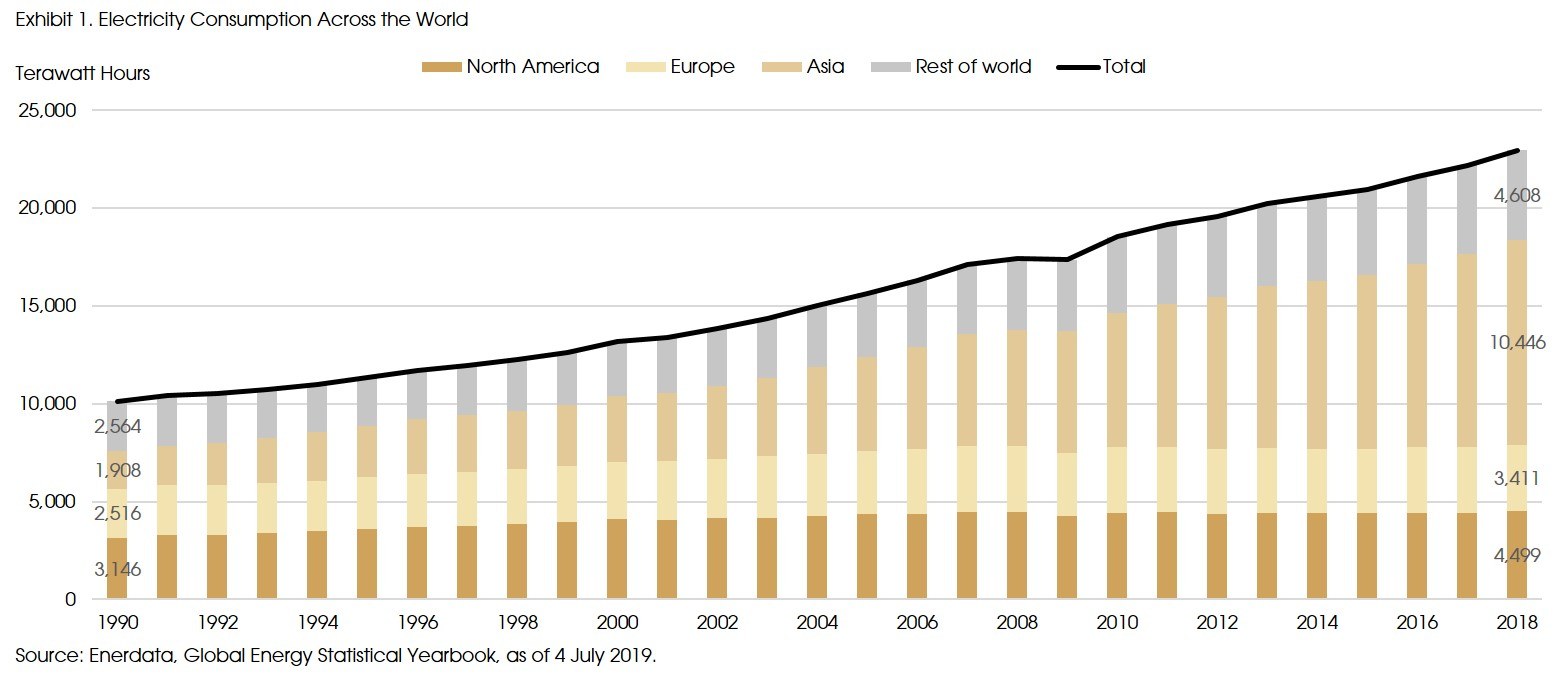

The growing global population in combination with greater urbanization and digitalization is leading to a continuous increase in demand for electricity. As can be seen in the graph below, the demand for energy in terawatt hours has almost consistently increased since 1990. 2009 is the only exception due to the Global Financial Crisis.

As shown in the above graph, the increase in electricity consumption is prevalent throughout the World. The developed regions, namely, North America and Europe, experienced a slightly slower growth of electricity consumption with an average annual growth rate of around 0.5% and 0.8% respectively for the period between 2000 and 2018. Asia has seen the greatest increase in electricity consumption with an average annual growth rate of around 7%. 2018 electricity consumption is over five times 1990 consumption in Asia. This can mainly be attributed by the economic growth experienced within the region, particularly in China and India. This growth in electricity consumption will continue. According to Scientific American, the global demand for energy will increase by no less than 50% over the next ten years and will double by 2050.

Current Renewable Energy Capacity

With ever-growing activism against climate change and reducing man-made greenhouse gases, the call for renewable clean energy investment is advancing. Although this call has been around for over 20 years, we are still at the ramp up phase with a lot of room for growth.

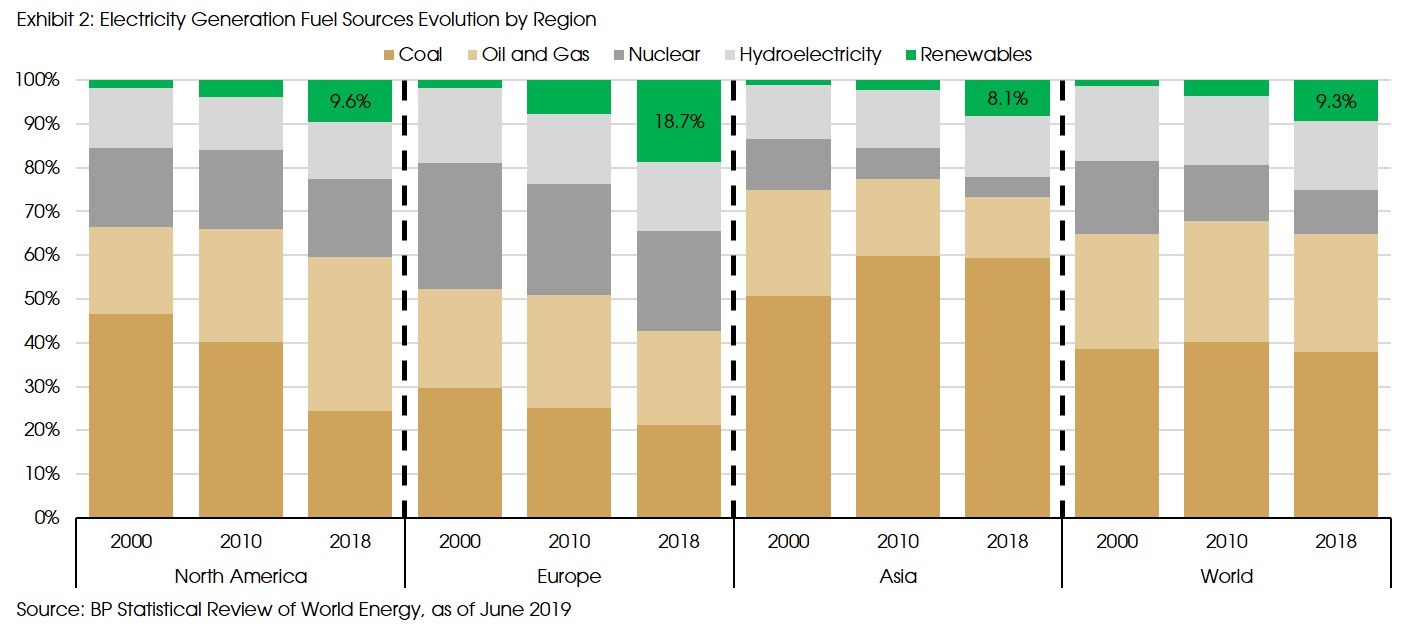

In the graph above, we can see that as of 2018, renewable energy, excluding hydroelectricity, is still a small portion of electricity production. We have excluded hydroelectricity, because it is increasingly viewed upon negatively due to the greenhouse gas emissions released from building dams, and the impact that damming has on wildlife and the water cycle.

Europe is at the forefront on renewables, with 18.7% of energy generated from renewable energy, North America and Asia are still quite behind with 9.6% and 8.1% respectively. For all three regions, over 70% of the renewable energy is generated from wind and solar energy. Wind energy typically accounts for around 50% of renewable energy generated, while solar is smaller at around 20%. However, the growth in solar energy generation has increased exponentially over the past three to five years as costs and technology improvements have been made.

This highlights that even though a lot of investments have already taken place in the renewable energy front, we are still near the beginning of the growth story. The demand for renewable energy will likely increase and grow at a rapid rate over the next decade. Currently, international agencies have a few estimates on the growth rate over the next decade. These are based on the National Determined Contributions (NDCs) which was signed by 197 member states of the United Nations Framework Convention on Climate Change in 2015. 2020 is a milestone year, because countries will review and update their NDCs. These reviews have not been conducted yet, but could lead to countries raising their ambition to scale up renewable energy. According to current NDCs, the global renewable power capacity is expected to increase 2.2 times from 2018 capacity by 2030.

Renewable Energy Growth Factors

Several factors have made renewable energy growth possible. In recent years, both public and political awareness of pollution and its potential consequence on both personal health and the planet has become more widespread. This has thus lead to demand from individuals, particularly millennials, to hold global corporations accountable in sourcing clean, sustainable materials for their products and energy. Governments in most regions are also placing greater environmental regulations and plans in place. These range from subsidizing renewable energy, electrification of heating, placing future target restrictions on the emissions of average cars sold in a region by carmakers thus encouraging the use and production of electric or hybrid cars, to the increasing phase out of coal power stations across the globe. The UK for example plans to phase out coal, which is the most polluting fuel, entirely by 2025, and is on track to hit that target ahead of time. In 2018, New Zealand already closed their last coal power station. The electrification of heating and transportation, on top of the continued phase out of fossil fuels will lead to a greater need for electricity as a whole, and electricity from a clean, renewable source to replace the pollutant emitting fossil fuels.

Moreover, political incentives on energy security and greater energy independence have also played a helping hand in advancing renewable energy. Geopolitical tensions with major oil producing countries in addition to renewable energy allowing countries to create their own electricity independently have increasingly made renewables an attractive option for policymakers.

Demand from global corporations has also powered renewable energy investments. Over 220 global corporations have already committed to going a hundred percent renewable in the near future. These companies include the large US tech companies: Apple, Google and Microsoft which have already shifted their data centers to be 100% powered by renewable energy. Apple is also helping its manufacturing partners to lower their carbon footprint by already installing 5 gigawatts of new clean energy sources, exceeding its goal of 4 gigawatts before 2020. Additional corporations on the list are from a wide range of sectors including Walmart, Unilever, Ikea, Starbucks, Sony, Diageo and HSBC. This shows that regardless of decisions by politicians, these global corporations, both publically listed and private are committed to the shift towards clean energy.

Investors are also increasingly taking into account ESG factors in their investment decisions, as highlighted in our previous Focus. This may place stronger pressure on publically listed companies in particular to stick to their clean energy commitments or place more stringent commitments to appease investors. Giant money managers like BlackRock and State Street are starting to divest from companies that emit excessive carbon like coal producers and oil E&P companies. Norway’s Government Pension Fund, the World’s largest sovereign wealth fund at over USD1 trillion in assets, announced in 2019 it would divest from oil and gas companies unless these had significant renewable divisions such as BP and Shell. This was particularly notable because the fund was set up in 1990 specifically to invest in Norway’s oilfields. The Church of England Pensions Board, which manages around $3.7 billion, also recently announced the launch of an index that rewards companies working to curb their carbon-dioxide emissions in line with the targets of the 2015 Paris agreement, and bars companies that fall short.

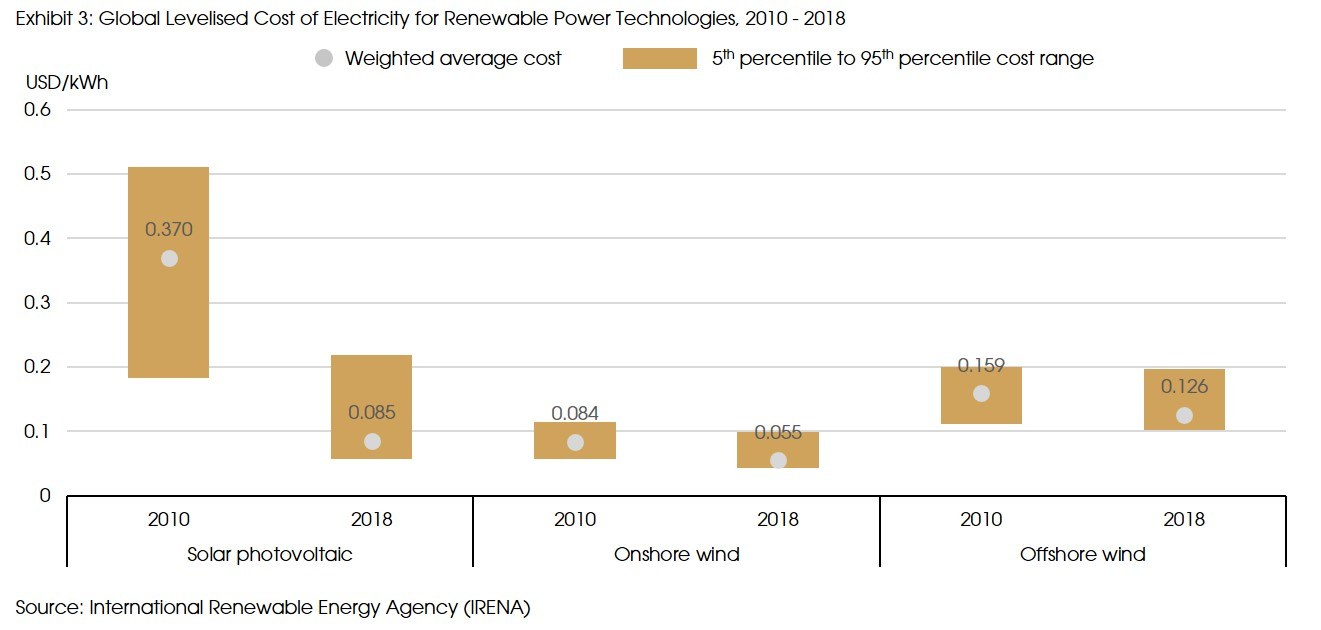

A final factor, and which may be the most important, is that technological advancements have made renewable energy more affordable. This is indicated in the graph below which shows the global levelised cost of electricity for renewable power technologies from 2010 to 2018. In the graph below, we highlight the cost of three renewable power technologies, solar photovoltaic, onshore wind and offshore wind, which are currently the most popular options. Within the short period of eight years, huge advancements have been made, particularly in solar photovoltaic technology. To put the advancements in perspective, in 2020, the cost of solar energy is roughly one quarter the costs projected by the International Energy Agency [IEA] in 2010. It has reached prices that the IEA’s 2014 solar roadmap did not expect until after 2050.

Solar photovoltaic energy and wind energy, both onshore and offshore, are becoming increasingly competitive on a pure economic basis, even without government subsidies. Estimates by McKinsey suggest that by 2030, solar and wind capacity will be cheaper than existing coal or gas plants globally.

These technological advancements make renewable energy a lot more competitive. As a concrete example, in September 2019, the Los Angeles Department of Power and Water signed a deal for 400 megawatts of power supplied by solar energy-plus batteries for a cost of 3.3 cents per kilowatt-hour (kWh]. This is almost half the estimated cost for a new natural gas plant which is estimated to cost 6 cents per kWh. Additionally, new power contracts are now being signed for 1.5 to 1.6 cents per kWh in sunny regions, such as Portugal and Qatar. Therefore, it is not just government regulations but also financial pressures leading to the construction of renewable energy plants.

Renewable Energy Investment Opportunities

Since it is indisputable that renewable energy will grow, the question is how best to invest in this energy revolution. The sector has had a relatively volatile history with companies going bankrupt, large swings from changes in political policies and winners and losers based on technological advancements. From the many potential avenues, we have identified three main types of companies to invest in which can benefit from the renewable energy trend. Two are relatively common options, the third is a relatively new structure which we will delve into greater detail.

Utility companies

Utility companies provide electricity to their customers and are usually considered relatively defensive, stable income-generating options for investors. At the moment, the majority of utility companies are still generating a large portion of their electricity from fossil fuels. There are a few though that are investing heavily into renewables. We therefore favour utility companies that prioritize renewable energy.

In particular, we like a utility company which we believe has become a leader in the provision of both wind and solar power. The company has a strong execution reputation with continued infrastructure investment. It is continuously investing into generating new renewable energy plants and large-scale battery storage which will advance its renewable energy generating abilities even further.

Renewable energy component manufacturers and installers

These include companies that construct a range of renewable energy components including solar panels, wind turbines or battery technology and storage. We believe that these companies require strong management which places priority on research and development. Renewable energy technology is still fairly new with improvements and new ideas constantly popping up. Solar and wind are currently the most popular forms and generate energy from nature. Fossil fuels can generate electricity consistently, but renewable energy cannot. Solar energy requires there to be sunlight and wind energy requires there to be a certain level of wind. Therefore, both solar and wind can be constrained during certain seasons, regions and time of day. Therefore, it is vital that the technology continues to improve, particularly in energy storage, to ensure that the supply of electricity from these sources can be more reliable and consistent.

Revenue prospects from these corporations can be highly variable. This is due to demand changes from technology discoveries and competition. During economic downturns or slowdowns, revenue and earnings for these companies may also be hampered as the construction of new solar and wind farms declines. So, overall we believe that this may be the riskiest form of renewable energy investment.

Yieldco

A yieldco is a relatively new investment structure that started in 2012. It is typically a spin-off or subsidiary of a utility company or a company that constructs renewable energy plants. Some additional terms that are required to better understand yieldcos:

- Sponsor – This is the utility company or renewable energy plant construction company which spun-off the yieldco. The Sponsor is also typically the majority stakeholder of the yieldco.

- Power purchase agreement [PPA] – This is an agreement negotiated before the construction of a power plant and have a typical contract period of around 15 to 30 years. These PPAs typically specify a fixed or inflation-indexed price.

The yieldco will purchase fully operational renewable energy plants with a PPA in place from their sponsor or other renewable energy plant constructors. Therefore, the future cash flow of a yieldco should be relatively predictable. Yieldcos act similarly to REITs and pay out most of their distributable income to shareholders. Therefore, due to the recurring nature of energy consumption and the fact that prices are set in place through PPAs, in theory yielcos should allow investors to receive stable generous dividend yields and also long-term dividend growth. Yieldcos were set up to provide an option for the sponsor to recoup the costs of building the renewable energy projects. On top of this, the sponsors can benefit from future cash flows generated by those projects through dividends from the yieldco. Therefore, yieldcos should be a great investment for investors seeking a stable income generating product. Yieldcos currently have an average dividend yield of around 5 to 7%. This should be a definite incentive for long-term income-seeking investors, particularly in the current lower for longer interest rate environment.

However, these investments do come with risks. A main one is corporate governance. Similar to all capital intensive, fast-growing sectors, there is a risk that the company tries to grow too quickly. This happened to SunEdison and their two yieldcos Terraform Power and Terraform Global. The same management team ran both SunEdison and the two yieldcos. SunEdison went bankrupt in 2016 after taking on over USD16bn in debt because they wanted to grow into one of the world’ largest solar power providers. The financial distress at SunEdison impacted the two yieldcos. Due to the lack of independent oversight, management was able to force the yieldcos to overpay for renewable assets. Consequently, this led to these yieldcos also taking on dangerous levels of debt. This combination of short-sighted thinking, as well as lack of independent oversight from the yieldco’s management teams, had both yieldcos on the verge of bankruptcy as well.

Post this incident, there was a major correction in valuation in most yieldcos as investors became aware of the corporate governance risks. Improvements have already been made within individual yieldcos. This was mainly done by increasing the number of independent directors within the board. This has led to a reduction in corporate governance risks, however does not eliminate it completely.

Another risk with yieldcos is the constant need for external growth capital. Yieldcos constantly need to raise cash in order to continue purchasing new renewable plants, as majority of the cashflow from their current plants go to shareholders. This means that these companies are often at the mercy of investor sentiment. Particularly if the share price is too low, it can result in a lack of the growth capital needed to acquire its sponsor’s assets and grow their dividends at rates investors expect.

Overall, we view this as an interesting option for investors seeking a relatively stable income-generating investment. The product is also backed by a strong growth story, renewable energy. In order to invest in these types of structures one would need greater comfort in the corporate governance practices of the sponsors. There are a few sponsors though that have a strong history of good corporate governance practices that are worth tracking.

Conclusion

In conclusion, we believe there is going to continue to be a shift in the energy market with winners and losers. The pressure from governments, through regulations and international agreements, large corporations and individuals, through consumer choice and responsible investing, will power this renewable energy revolution. Moreover, the continued electrification and phase out of fossil fuels will continue to contribute to this trend.

Although vast improvements in renewable energy technology have been made, more still needs to be done to in both generating energy and battery storage to ensure that renewables can become even more efficient and dependable globally. We believe that the current low rate environment as well as political priorities within certain regions may make the current moment a strong turning point for the growing acceptance of renewable energy. All in all, though, as always, we advocate for active selection, strong due diligence, prudence and care when investing in the renewable energy growth story.

Sources: Absolute Return Partners, Bank of America Merrill Lynch, Bloomberg, BP Statistical Review, Enerdata, Frankfurt School United Nations Environment Protection Collaborating Centre, Greentech Media, Intelligent Income, International Energy Agency, International Renewable Energy Agency, Mckinsey & Co., Pimco Investments, RE100, Scientific American, The Financial Times, The One Brief, The Wall Street Journal, and CIGP Estimates.