Focus: Approach to Responsible Investing

Guillaume Page

Our world and financial markets have consistently changed and moved together over the last century, driven by mega-trends, shift in powers, revolutions and the rise of technologies. As we are facing crucial environmental and social challenges, the financial world has seen the emergence of a new trend, namely sustainability-oriented responsible investing. It is a common question today to estimate if this trend will really influence and reshape the financial industry and be a major force for the next decade, as passive investing has been for the past decade.

Responsible investing has been linked to many concepts and approaches such as Principally Responsible Investing (PRI), ESG Investing, Impact Investing, and Socially Responsible Investing (SRI). As there is no clear formal definition of these terms, we believe a large number of industry practitioners often confuse such strategy and it is important in our view to clearly understand these concepts.

Policies and organization guidelines are shaping more and more the practice around responsible investing. As an important step in responsible investing trend, in 2006 the United Nations has developed and launched the Principles for Responsible Investment (PRI) consisted of six principles with the mission to frame an economically efficient, sustainable global financial system.

The PRI defines responsible investment as a strategy and practice to incorporate environmental, social, and governance (ESG) factors in investment decisions and active ownership.

Based on our encounters talking about the subject, more often than not, when referring to sustainable / ESG investing, most people are essentially referring to the broader sense of the concept. We believe this is somewhat closely related to what UN PRI is trying to define. Hence our preference to adhere by this very definition.

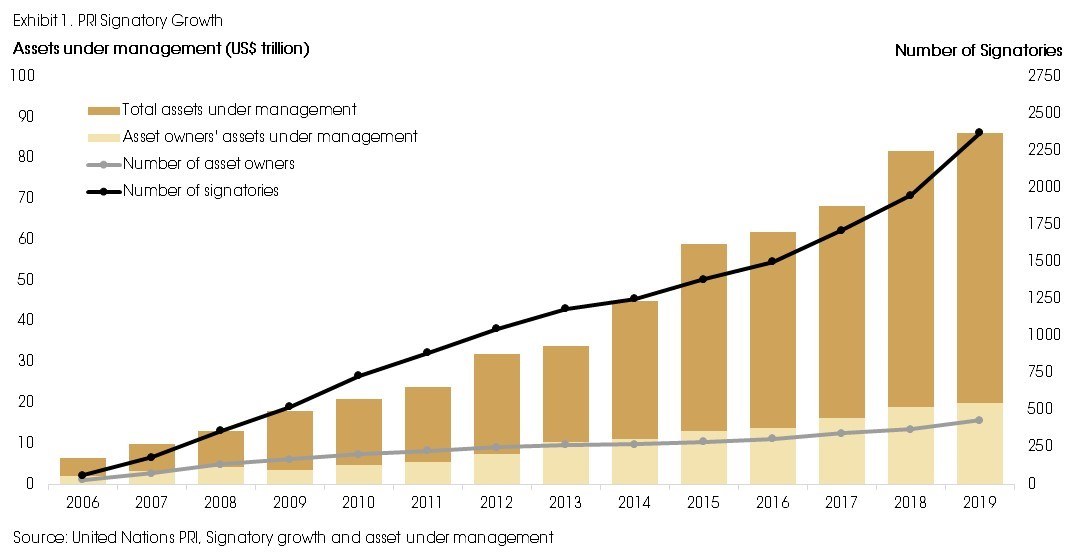

Since 2012, the number of signatories has grown from 1,050 to almost 2,400 funds, a group that controls USD 86 trillion in capital. Those funds, a mix of institutional investors and fund managers, have committed to six principles, including a pledge to incorporate ESG issues into how they choose and manage investments. In 2015, all UN member states also adopted 17 Sustainable Development Goals (SDGs) with a 15-year plan to achieve these goals, which aim to end poverty, protect the planet and improve people’s life. A combination of the 17 SDGs are increasingly selected and used by impact fund manager for their thematic strategies.

Evolution of Responsible Investing

In the past years, a growing and diverse universe of investment opportunities have been offered to investors. The considerable growth in responsible investing trend is mainly driven by:

- A significant growth in demand from investors and clients, including from millennials, whose savings are growing and seek to invest in products in line with their values. According to Schroders 2019 Global Investor Study, which surveyed 25,000 investors worldwide, more than 60% of those under the age of 71 believe that all investment funds should consider sustainability factors when making investments.

- A constant focus and growing awareness on challenges around sustainability.

- As technologies and data analysis are improving, market participants can have access to more accurate data and have better understanding of numbers.

- New regulations around responsible investing through mediums such as ESG Reporting.

The responsible investing trend is not only supported by investors worried about social and environmental issues but also helped by growing evidence that incorporating factors such as ESG criteria in investment selection could actually improve risk-adjusted returns and improve risk management exposure. This is an important factor from a risk-return perspective, not necessarily higher absolute return.

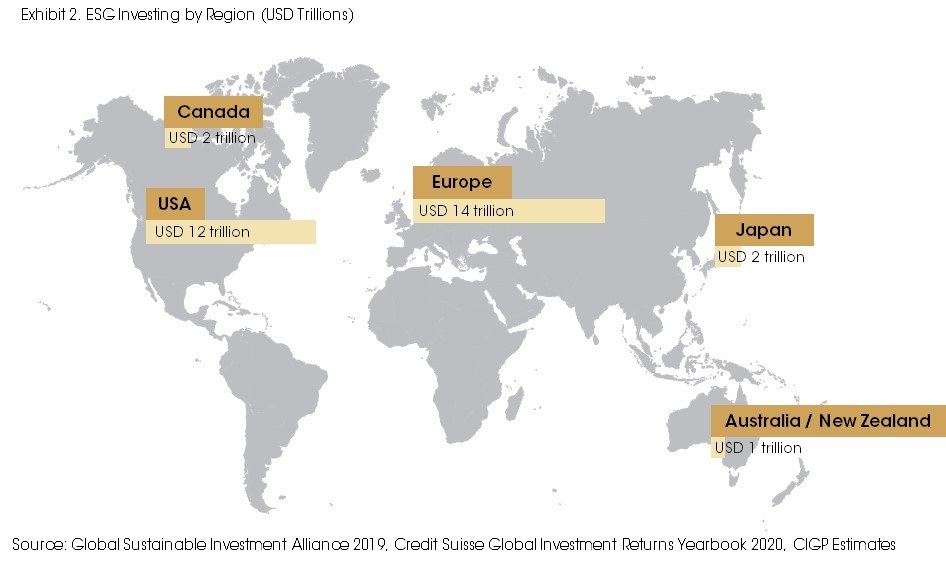

According to Credit Suisse, investment products linked to ESG criteria had a total value of USD 31 trillion in 2018, a 34% increase over two years. Estimates for 2019 are leading to a market value of USD 40 trillion. While the leading ESG-oriented region is Europe, the trend is growing faster in the US.

World's biggest investment firm BlackRock and its CEO Larry Fink released early this year two public letters, one to CEOs and the other to clients, sharing their view on climate change and how climate issues are reshaping finance. For Blackrock, companies should disclose sustainability information in line with the Sustainable Accounting Standards Board (SASB) requirements and corporate reporting should be aligned to Task Force on Climate-related Financial Disclosures (TCFD) guidelines. Passive investing was the main trend this last decade with ever increasing amounts of products. ESG products and ETF integrating ESG could represent a large proportion of investment funds and portfolios in the coming years. For now, this market is relatively small but Blackrock showed the path as a strategic segment. There are now around 70 sustainable ETFs up from 25 in 2016.

Another important growing segment of sustainable products are Green bonds. Most of these bonds are focusing on energy efficiency and lower carbon transition of the company issuing the bond. In 2018, a record USD 167 billion in green bonds were issued, and this market passed the USD 200bn barrier in October 2019.

Responsible Investing Process and Methodologies

The way to approach responsible investing can be very different from one investor to another, and it has already evolved significantly since the trend started. When looking at a company, funds and investors usually base their strategy using one of the following main approach:

- ESG risk-return optimisation: this method consists of using ESG factors while screening investment opportunities and optimising portfolio’s return on a risk-adjusted basis. Some common factors are carbon footprint, human rights or employee relations and can vary between companies and sectors. Investments can be graded and ranked following the ratings of specialised rating agencies and/or ESG factors are incorporated into the valuation model of the company.

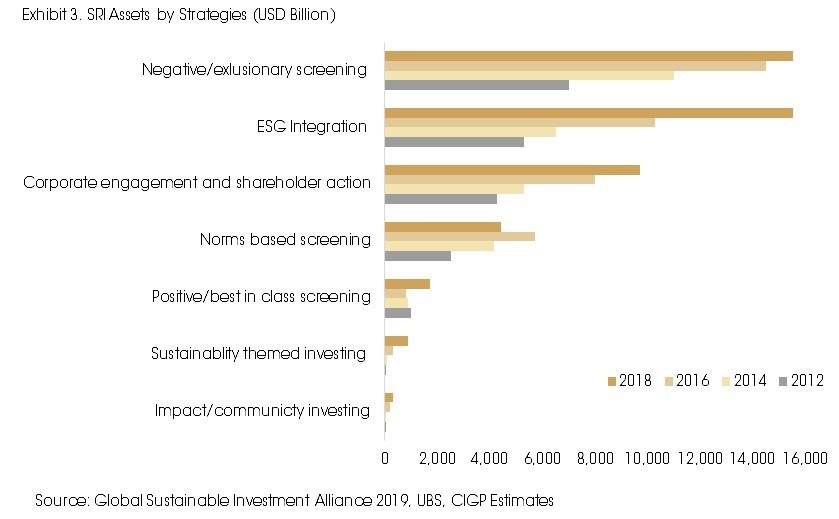

- Negative screening or exclusions: the strategy will exclude companies which businesses are known to be harmful, in practice this translates into excluding sectors or companies with poor environmental and social records. Such a strategy prevents exposure to companies in conflict with investors/general public social objective (tobacco, arms, alcohol, fossil fuels).

- Positive inclusion: investors select only sectors/companies with positive impact through their products or services. They provide solutions for specific social and environmental challenges within a theme or trend (climate change, food sharing, food security, financial accessibility, social development).

Exclusion methods were the first one to appear and are still widely used. However, strategies focusing on ESG integration and positive inclusion had the highest growth in the past years. This evolution is probably due to a better understanding on how companies are evolving. Studies have shown that “bad/sin” sectors/companies do not necessarily underperform “positive impact” sectors over a certain period. “Sin” sectors usually are defensive sectors with high barriers to entry and monopoly power. These companies may also operate strategic decisions and improve their businesses, which lead to growth (ex. Oil and gas companies shifting to sustainable energies). By excluding some of these companies, investors might face costs of opportunities.

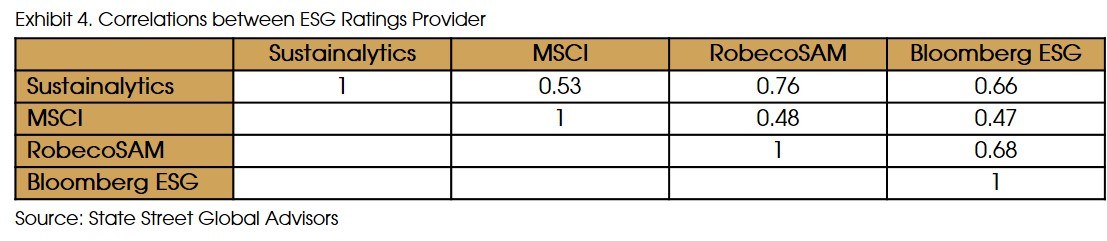

A majority of investors rely on external ESG rating agencies to score companies during their investment screening process. Analysing ESG factors require specific resources and knowledge and special rating agencies appear to be a common tool for investors. The main rating agencies are Sustainalytics, MSCI ESG, ISS Oekom, Arabesque S-Ray ESG, FTSE Rusell ESG and RobecoSAM. All agencies have their own methodologies when they analyse and score companies, and some focus only on specific factors.

Scores from rating agencies are useful for ESG risk-return optimization approach as they can easily give access to specific measures to investors. However, ratings have certain shortcomings and a range of inconsistencies exists between rating agencies. There is a clear lack of standardization and data disclosure limitations which lead to a diversity of metrics measuring the same attribute of a company. One famous example is Tesla which is rated as one of the best car manufacturer by MSCI as Tesla’s cars have “zero” carbon emission, while FTSE downgrade the company for Tesla production footprint. Rating agencies methodologies are also creating bias such as 1) company size bias - large cap companies have more resources to disclose ESG related information, 2) geographic bias - difference in regulatory reporting requirement across region, and 3) industry bias – difficulties to incorporate specific differences and risks for certain businesses.

Investors should be aware of these characteristics when selecting one or multiple ratings in their screening process as for now all market participant have different criteria and views on how to tackle ESG screenings. Similar to credit ratings, it will be a long path before there will be a more standardize and developed approach. However, this is necessary to improve the research and support the trend towards responsible investments.

Drivers and Challenges of Responsible Investing for the Future

More and more ESG strategies have ownership of known stocks and overweight stocks. For some stocks, these strategies already owns more than 10% of their floating shares. With the continuing growth of responsible investing and asset under management, share of ownership will increase further. This will put pressure on company’s management to keep a sustainable path and stay away from negative news affecting their company’s image.

As more and more responsible investing funds will own these stocks, they will represent a large group of investors and will potentially create large market movement whenever they decide or force to sell to comply with their strategies. Investors, who are not necessarily including ESG factors in their process, should pay more and more attention of these pressures and be cautious of the market changes created by this trend.

Moreover, companies and financial institutions should not neglect the potential rising social pressure on their shoulders. As more information is available nowadays, the general public can easily have access to information on unethical or unsustainable decisions made by a company and its board. Large institutional shareholders and financial institutions also have a responsibility in a sense that they can approve or not strategic decisions, and can also be under the spotlight when allowing companies to conduct such businesses. As the latest example, the German conglomerate Siemens has faced criticism by institutional investors and climate activists because of its role in a controversial Australian coal-mining project. Siemens was criticised for management’s lack of consideration for risks for the company and large institutional investor Blackrock was blamed for not actively disapproving Siemens’ decisions, just few weeks after the asset manager announced its willingness to put sustainability as a core part of its investment process. Such events are definitely negative publicity for companies and there is a growing concern and fear over them. Another example, JP Morgan recently announced that the bank will reduce significantly its revenues from advising and financing companies active in coal extraction and left room potentially for other sectors.

Companies in any sector need to emphasis their sustainable decisions and not underestimate potential impact of negative comments on their practices. In a study made in December 2019, Goldman Sachs Research looked at a broad universe of so called ESG related funds and formed a list of the top 50 widely owned stocks by these funds. The first two of the list are two large tech names, Alphabet Inc and Microsoft. The top 10 also included companies such as Allianz SE and AXA SA. It obviously does not take into account the size of investments but it gives an indication on the investment universe of these funds. More naturally linked sectors or companies related to E,S or G are not necessarily the most owned stocks for now.

Impact investment is the strategy type that invests in responsible and sustainable sectors. It is traditionally used in private markets, where investments are made for specific projects. For public market, it is categorised as sustainable thematic investments. This category is currently a small part of the whole responsible investing universe, however it is the category with the largest growth in the last three years. Growing demand and offer for sustainable thematic strategies do not come without risks. These strategies are focusing on a narrow investment universe of companies with sustainable businesses and products. This will probably result in some challenges for funds to create diversified and sizeable portfolios. From observations, impact funds are smaller and they are holding less positions compared to ESG strategies. The scarcity of investment opportunities is also benefiting best-in-class stocks as more inflows goes to impact funds, and will definitely push their valuation upward. We can expect that at some point in time the companies will have to justify inflated multiples, however these companies are generally active in sectors with growing and long-term perspective and more competition may appear in the coming years.

In addition, stricter regulations surrounding ESG disclosure and reporting will intensify and push regulated investors and companies to be more socially responsible and consider more ESG integration. ESG policies and regulations across global capital markets have increased from 430 in 2015 to 817 in 2019. Europe is the leading region in terms of ESG regulatory policies and proposals (65% of policies). With more in-depth and standardized regulations, investors will need to implement further ESG factors into investment process and focus more on ESG risks. Companies will need to disclose and prove their engagement on ESG issues. Deeper integration will also depend on the improvement of the quality and availability of ESG data and standardised requirement for corporate reporting. There will be challenges for smaller companies with less resources and coverage.

Overall, benefits from well-thought out rules will drive the whole financial industry to improve its resources and knowledge in being socially responsible. Some will be able to differentiate themselves through their strategies and grow their AUM. Policies will drive companies to disclose clearer ESG risks and report their engagement. We believe companies who manage to embrace successfully in this trend will attract long-term shareholders and help them manage potential pressure on their cost of capital.

Regulators have an important role to play when providing clear guidelines to market participants and helping them in their efforts towards being more responsibly compliant. Regulations across the world will need also to find an equal balance in their coverage as some participants outside a region might struggle to apply local rules.

The Private Equity world has seen less pressure on its participants from a regulation standpoint but there is a growing number of private equity firms which have started to rethink their approach, influenced in part by their Limited Partners (investors). For PE funds, the important question is, as in public markets, does sustainable/ESG investments provide better returns? It is probably too soon to have a clear view as the trend came later in private equity, but more examples and studies will arise and will help (or not) to keep the momentum driving the efforts. Returns in PE take more time (years) to be realised and it might also be challenging to measure what are the main contributors. PE funds will need to contribute efforts to put in place process that track ESG factors and related decisions, and have a clear understanding of their implication on their investments. It can also force more strategic decisions of PE investors in the company they invest in as they would work on improving all ESG aspects of the company, and not just act as a financial investor. If a large number of PE firms do these efforts, this will certainly improve the overall company. However, one risk would be that PE firms only select companies having already sustainable operation in place/or sustainable business. PE firms would not really add any value and pressure on the company to improve. Eventually, momentum of ESG investment in PE would be less impactful.

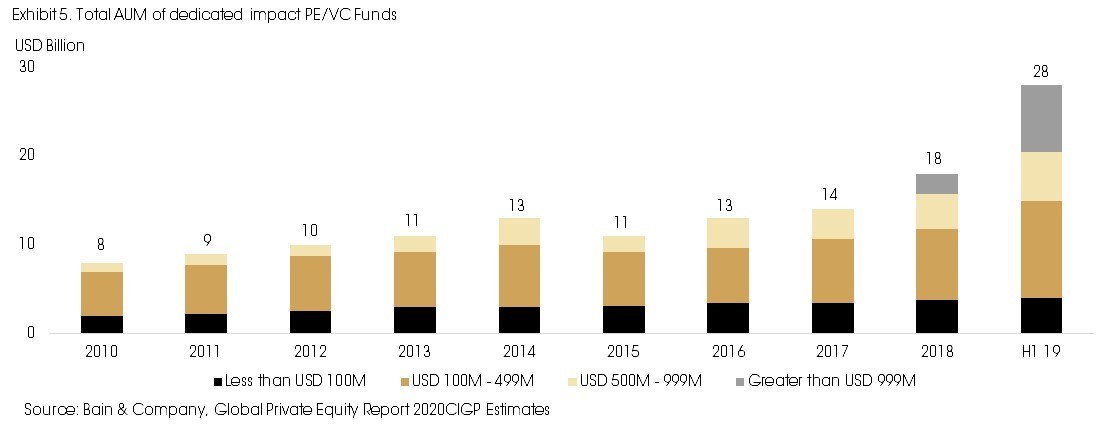

To identify and manage ESG risks and opportunities, GPs will need to develop new expertise or partnerships with specialised firms. ESG implementation could be difficult for small/medium PE funds as they won’t have the resources or partnerships to implement ESG integration on their process. For now, the trend has been more pronounced from specialised impact funds and large PE houses (mega funds). From 2015, assets raised by impact strategies have increased by 154% and reached USD 28 billion and observed a sharp growth in +1 billion funds in the last two years with example from TPG Rise Portfolio, KKR or Partners Group. These large firms have a strategic interest in entering the impact fund space as they can use existing resources and take advantage of ESG movement to attract more assets.

Opportunities for Investors and Shareholders

For investors, whether they are large/small financial institutions or even individuals, the evolving trend towards responsible investing is giving them new opportunities to adapt the way they look at the world and companies. It is necessary to grow an in-depth awareness of new factors influencing positively and/or negatively the whole investment universe and investors shall realise the central role they can play. Overall, it exists a general consensus who believes that sustainable investing can generate above-average performance.

There is obviously no plug-and-play and perfect approach. There are certainly a variety of methodologies that will be implemented depending on diverse views and values, and not all the different players have the same resources and goals. In our intellectual reflection, we have recently focused on defining our approach based on our investment philosophy which comes close to the concept of “Shared Value”. The concept was defined in an article by Professor Michael Porter and Mark Kramer in the Harvard Business Review (“Creating Shared Value”, January/February 2011).

Companies put in place a business strategy with policies and practices that focus on having measurable economic benefits while addressing social/environmental aspects that influence their business. For companies, the main goals of the shared value strategy is to differentiate themselves from their competitors, achieve structural efficiencies and offer better value to existing/new customers. As defined by Michael Porter, the three main pillars of the strategy are 1) products/services focusing on new social needs or new customers, 2) improve the efficiency and productivity of the whole supply chain of the company, and 3) enhance the business environment where the company operates. Example can be either when sports apparel companies Nike and Adidas are producing shoes with zero waste and made of reused plastic, or when Walmart is working with +1000 suppliers to eliminate significantly carbon emission and save costs.

The majority of used ESG criteria are not covering the link between companies’ social and environmental actions with their actual business and its environment. As a simple example, the bank JP Morgan can disclose less carbon footprint and receive a high rate based on ESG criteria, when in reality it does not improve necessarily the bank’s profitability nor have a significant impact on carbon emissions globally. Shared Value strategy are thus more effective in theory to help solve challenges across the world.

Shared value put also the responsibility on companies’ management and governance as to implement it effectively as a core strategic plan for and throughout the whole company. In general, whether using ESG criteria or not, the “G” factor is what matters the most at the end. It is only with great governance and leadership that a company can address the social and environmental issues related to their business. Today, a majority of criteria on governance are focusing on aspects such as the remuneration of board directors. Those are obviously fair points but not the most important ones to drive companies’ sustainable and impactful performance.

As part of our fundamental research, we aim to find and invest in companies that have business strategies with long-term competitive advantages. The combination of shared value and traditional financial analysis has definitely the potential to bring value for long-term investors.

Another way market participants can combine successfully responsible investment and returns is through active ownership. By engaging more and collaborating more among them, investors’ contributions can influence the companies’ goals and performance towards sustainable practices. Shareholders have tools such as collaborative engagements or voting rights to interact with companies’ management. It obviously requires a large and united club of investors, but public companies simply cannot neglect the involvement and decisions of large investors and potential impact on the cost of capital of companies. Good co-operation between active owners and companies has shown significant financial and non-financial results as it ultimately increase companies’ value.

Conclusion

In conclusion, we believe the trend of responsible investing will move from a trend to a normality in the next two decades. Based on the different initiatives taken across regions and stakeholders, there is a growing and significant force that is driving the evolution of responsible investing. Some market participants are obviously taking advantage of the trend and take part of it for strategic reasons as it opens opportunities.

In our view, it is important that growing inflows of assets should be bolstered by more market awareness and more transparency. Regulations around the world will have a key role to play in order to shape practices that are more efficient. Moreover, with the shift towards impact investing and thematic sustainable funds, it will be interesting to observe if such strategies do really outperform and bring up companies with positive and impactful businesses.

As companies and the financial industry are facing social pressures, more demanding clients (investors) and customers, they will need to comply with new standards when it comes to disclosing information to stakeholders. We believe talented and engaged management can take advantage of these changes and drive their companies’ values higher. As we said, there are different ways to approach responsible investing and probably numerous of them have successful impact and performance. The concept of Shared Value is one of them and we think combining it with traditional fundamental research could be beneficial for long term investors who are investing in quality and sustainable businesses.

Sources: Bain & Co, Credit Suisse, Global Sustainable Investment Alliance, Goldman Sachs Research, Jefferies, Triodios Investment Management, UBS Investment Research and United Nations PRI.