CIO Viewpoint: Chase the Stock or Own the Stock

The equity market bull run accelerated in 2015, having begun in 2009, and now has extended through 2019. It has been one of the longest runs in history. In late 2018, however, US stocks crashed when US Federal Reserve Chairman Powell said in a speech that the Federal Reserve had “arrived at the lower end of neutral rates” implying that rate increases would not be forthcoming. This spooked investors and stocks, which typically rise on lower rates due to lower borrowing costs. Equities sold off. The S&P 500 ended 2018 down approximately 6% and the EuroStoxx 50 ended down approximately 15%. The probability of two rate cuts in 2020 seems to be the consensus at this juncture. This is likely to be supportive to stocks. Year to date (YTD), most equity indices are up double digits due to several reasons. Some of these include: (1) continued expectations of easy monetary policy, (2) potential for broader fiscal stimulus, (3) constructive corporate fundamentals and (4) lack of investment alternatives for appreciation and yield.

3 reasons why we are still overweight equities:

- The equity risk premium in the US is still attractive, but 2020 earnings will be key to that trajectory.

- Corporate fundamentals remain constructive.

- The risk reward for stocks versus other asset classes is still attractive.

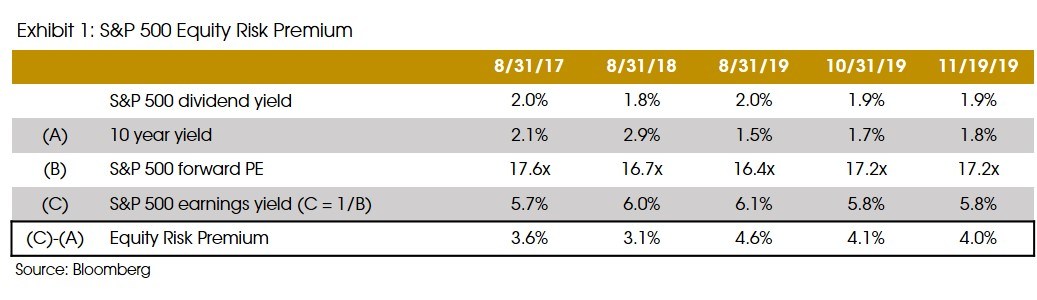

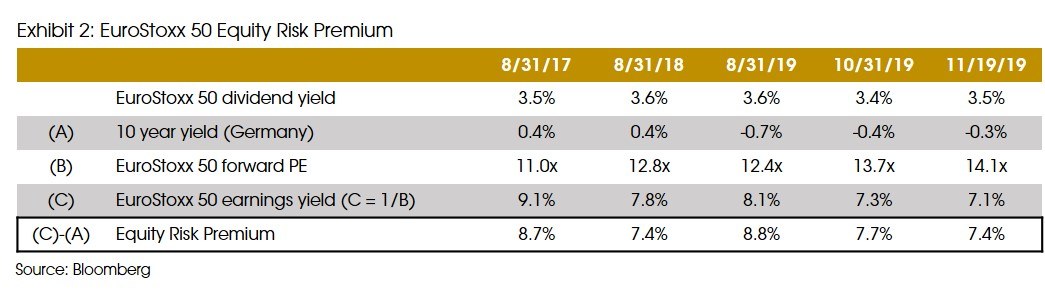

The Equity Risk Premium

Evaluating if investors are being compensated for the risks of owning equities versus other asset classes is an important asset allocation exercise in respect to the equity risk premium equation. In Europe, investors are clearly still buying equities, as evidenced by the stellar index performance. We think European investors remain bullish through 2020, largely because of central bank policy which effectively purports a negative rate environment for the foreseeable future. In the US, a still relatively supportive macro environment is propelling stocks.

Fundamentals over Momentum

Our preference in equities is for fundamentally based investment decision making. As long term investors we stick to our approach of identifying well run companies, reasonable valuations, predictable business models, and evaluating a series of long terms catalysts and secular tailwinds that can result in an overall portfolio of stocks that could weather different cycles.

US

Specifically, in respect to stock prices, both the technology sector (+40.21% YTD) and healthcare sector (+12.75% YTD) in the US have seen significant price gains in 2019. We like both technology and healthcare as core long term allocations. However, we see some risk as the 2020 US presidential election campaign gains headline space in the market’s narrative. [See our June Viewpoint: Anti-Trust or Anti-Tech. Contact us for our best ideas.]

Europe

Extended monetary policy accommodation by the European Central Bank has been the main precipitator of bringing European indices to new highs with all indices up greater the 20% YTD, except the UK. Low rates and limited yield alternatives for Euro denominated investors have likely forced portfolio migration to an overweight in stocks. While this has paid off through YTD returns, there may be more underlying risks than there are the US in the event of a flash crash. Germany’s narrow avoidance of a technical recession seems to have produced optimism, albeit likely to be temporary. Here again, macro policy is likely driving the momentum trade.

Risk - Reward: Trade-off for the Best at the Moment

It was only a year ago when markets were expecting and pricing in a US recession mid-to-late 2019. Obviously this has not materialized, but the recession rhetoric remains. The yield curve has steepened only just a little of late which has warded off some of the more aggressive recession talk in the markets. However, there is concern that markets could literally talk themselves into a recession. This risk is all too great given the fragility of the equity markets.

Exhibit 3 shows ten year projected asset class returns, according to Allianz Global Investors. As we think about our asset allocation positioning for the long term, we consider expected returns and expected volatility, among other factors, across various assets class and their sub parts. This helps to build diversified all-weather portfolios that preserve capital but also incorporate appreciation and income. We couple this with the long-term policy view of global central banks.

What to Do

We remain overweight to equites due to constructive fundamentals, reasonable equity risk premium and risk reward vs other asset class. We feel equites are adequately attractive to hold in this environment with some room for upside as earnings growth expectations continue to be priced into the market. As we discussed in our October Viewpoint: International Wall of Worry we’d look for a sustained deterioration in consumer sentiment, for example.

We still prefer fundamentals over momentum and liquidity. We do not suggest chasing stocks or sectors. It’s too early to bet on the likely outcome of the US 2020 presidential election much less betting on the outcome of a trade deal.

Uncertainty remains and it’s important to stay diversified through year end and into 2020 as the trade negotiations continue to weigh on markets. Broad and diversified portfolios, balancing both risk and reward across asset class, sector, region and currency will help to weather flash crashes that could prolong into extended down weeks in the markets. Talk of recession may heat up and could be the cap to what is needed to reset investor mindsets.

As always, active and prudent portfolio management to stay on top of the ever changing dynamics will help to preserve capital in portfolios.

Sources: Allianz Global Investors, Bank of Singapore, Bloomberg, DBS, Factset, Julius Baer, Lombard Odier, Picet, Reuters, S&P Global, The Federalist, The Financial Times, The New York Times, and Wall Street Journal.